Generational Wealth Transfer and Your Estate Plan

Protecting your family’s legacy so that it lasts for generations requires more than just a simple will — it requires careful planning and open communication. Each generation views the world differently, which can create competing priorities about how wealth should be used.

Today’s Millennials and Generation Xers often have different values than their parents and grandparents, placing greater emphasis on sustainability, climate action, and lifestyle choices rather than pure wealth accumulation. How can you guide your family’s financial decisions long after you are gone?

It starts with understanding the scope of the largest wealth transfer in history — and making a plan.

The Largest Wealth Transfer in History

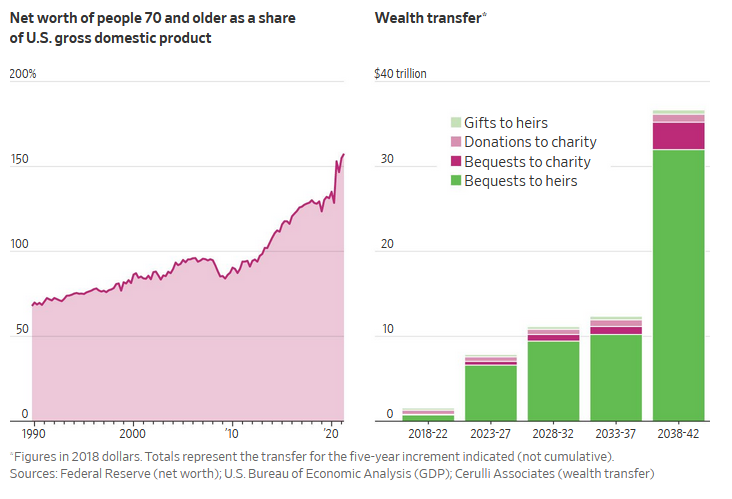

According to The Wall Street Journal, between 2018 and 2042, roughly $70 trillion will be redistributed in the United States. About $61 trillion of that will pass directly to heirs, while the rest will flow into charitable giving. This massive shift underscores the economic influence of the Baby Boomer generation, who came of age in post-World War II prosperity and have driven the U.S. economy throughout their lives.

Many benefactors are not waiting until death to transfer wealth. Lifetime gifting is increasing, with the IRS reporting steady growth in taxable gifts each year — and that number represents only a fraction of wealth transferred outside of the tax system. This early transfer of wealth is already fueling economic activity, allowing recipients to:

- Purchase homes

- Start businesses

- Donate to charitable causes

- Create family foundations or other wealth-sheltering structures

The Financial Literacy Gap

Despite this historic wealth transfer, younger generations often lack the tools to manage it wisely.

- The TIAA Institute reports that only 11% of Millennials have “relatively high” financial literacy.

- Nearly 28% of Millennials report “very low” financial literacy.

- Generation X struggles as well, particularly with long-term saving and spending habits.

Without proper guidance, inheritance money may be spent quickly on daily expenses, vacations, paying off debt, or medical bills — rather than preserved to benefit multiple generations.

Talking About Wealth Without Creating Conflict

One of the most powerful steps you can take is having open conversations with your heirs. Yet many families avoid these discussions out of fear.

- Parents and grandparents often worry that revealing the size of an inheritance will remove motivation or work ethic.

- Children and grandchildren sometimes withhold financial information from older generations to avoid perceptions of favoritism in future gifts.

Clear communication helps bridge this gap and prevents surprises. Your estate plan can also include language and structures that encourage responsible stewardship, such as incentives for education, work, or charitable giving.

Smart Financial Tools for Multigenerational Wealth

Beyond 529s and Custodial Accounts

While 529 plans and UTMA/UGMA accounts are common ways to save for a child’s future, they may not always be ideal.

- These accounts typically transfer outright to the child at age 18 or 21 — regardless of maturity level.

- If the child receives a scholarship or decides not to attend college, funds may be redirected with tax consequences.

- If the child faces addiction, debt, or other challenges, assets could quickly be depleted.

Consider a Gift Trust

An estate planning attorney may recommend creating a gift trust for a newborn or young family member.

- Offers similar tax-free growth benefits

- Protects assets from misuse or creditors

- Allows the grantor to pay taxes on behalf of the trust

- Can include specific instructions for when and how funds are distributed

Revocable Living Trusts (RLTs)

You can also create a revocable living trust that includes children, grandchildren, and future generations.

- Allows for centralized management of family wealth

- Can be amended as the family grows or circumstances change

- May direct beneficiaries to establish their own trusts to keep the planning going

Keeping the Plan Current

The best multigenerational estate plans are living documents that evolve over time.

- Revisit your plan regularly with your estate planning attorney

- Update for life events — births, marriages, divorces, or deaths

- Adjust for changes in tax law or state regulations

A proactive, regularly updated plan will ensure that your wealth continues to serve your family’s needs for decades to come.

Protect Your Legacy — Start Planning Today

Generational wealth planning is about more than money — it’s about values, guidance, and family harmony. By working with an experienced estate planning attorney, you can:

- Preserve your assets

- Provide for heirs responsibly

- Reduce taxes and avoid unnecessary probate

- Encourage responsible stewardship of wealth for generations to come

Call us at (207) 848-5600 or visit our Contact Page to start building your family’s legacy plan today.